State of Student Aid in Texas – 2021

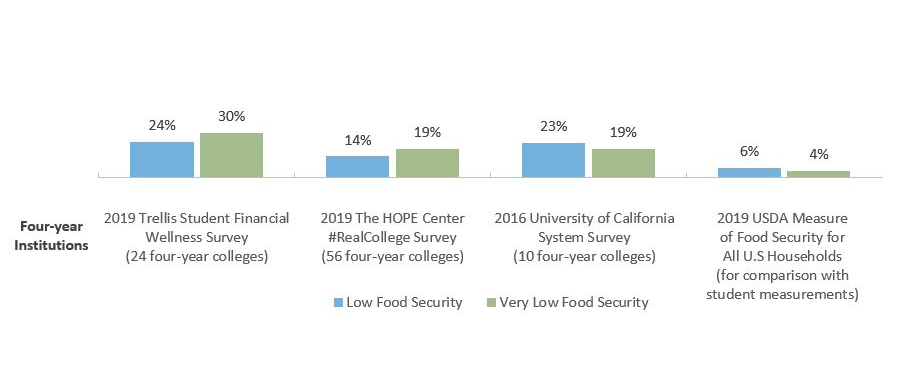

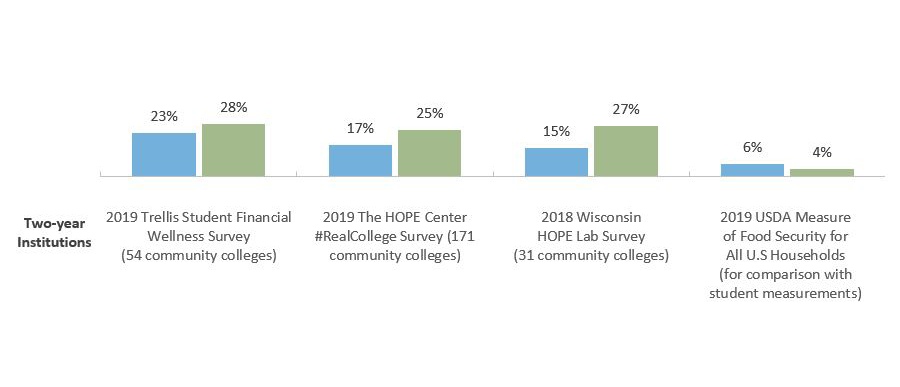

Recent Studies of Food Security Amongst College Students Find Similar, High Levels of Food Insecurity

Recent Studies of Food Security Amongst College Students Using the U.S. Department of Agriculture Scale

Note: The Trellis survey used the condensed six-question food security scale while the other surveys used the 10-question version.

Sources: United States Department of Agriculture (USDA). 2017. Definitions of food security. (https://www.ers.usda.gov/topics/food-nutrition-assistance/food-security-in-the-us/definitions-of-food-security/); Klepfer, K. Cornett, A. Fletcher, C. & Webster, J. Student Financial Wellness Survey: Fall 2019 (https://www.trelliscompany.org/student-finance-survey/); Baker-Smith, C. Coca, V. Goldrick-Rab, S. Looker, E. Richardson, B. & Williams, T. (2020). #RealCollege 2020: Five Years of Evidence on Campus Basic Needs Insecurity. The HOPE Center for College, Community, and Justice. (https://hope4college.com/wp-content/uploads/2020/02/2019_RealCollege_Survey_Report.pdf); Baker, Goldrick-Rab, S., Richardson, J., Schneider, J., Hernandez, A., & Cady, C. (2018). Still Hungry and Homeless in College. Wisconsin HOPE Lab. (https://hope4college.com/wp-content/uploads/2018/09/Wisconsin-HOPE-Lab-Still-Hungry-and-Homeless.pdf); Martinez, S., Maynard, K., & Ritchie, L. (2016). Student food access and security study. University of California Global Food Initiative. (http://regents.universityofcalifornia.edu/regmeet/july16/e1attach.pdf); U.S. Department of Agriculture, Economic Research Service. Food Security in the U.S. (https://www.ers.usda.gov/topics/food-nutrition-assistance/food-security-in-the-us/key-statistics-graphics/).

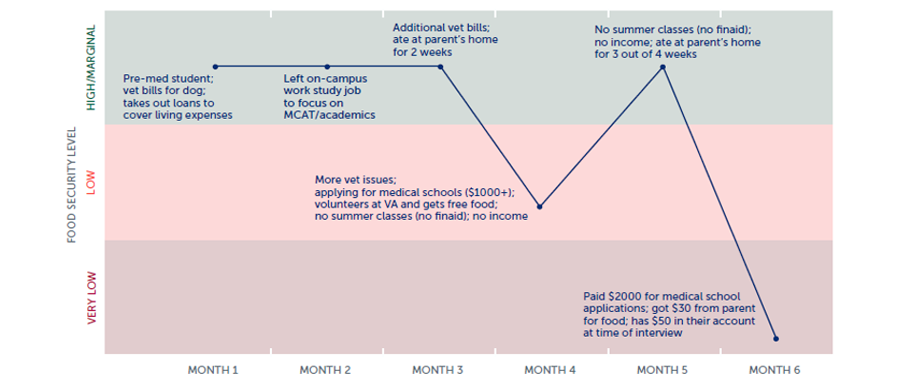

Longitudinal Study of College Students Reveals Fluid Pattern of Food Security

*Researchers are unable to rule out the possibility that declining food security may be explained, in part, by the subjects becoming more comfortable discussing this sensitive topic with interviewers.

Sources: Cornett, A., & Webster, J. (2020). Longitudinal Fluidity in Collegiate Food Security: Disruptions, Restoration, and Its Drivers. Trellis Company. Retrieved from: https://www.trelliscompany.org/wp-content/uploads/2020/02/Research-Brief_FSS_Longitudinal-Fluidity.pdf; Fernandez, C., Webster, J., & Cornett, A. (2019). Studying on Empty: A Qualitative Study of Low Food Security among College Students. Trellis Company. Retrieved from: https://www.trelliscompany.org/wp-content/uploads/2019/09/Studying-on-Empty.pdf

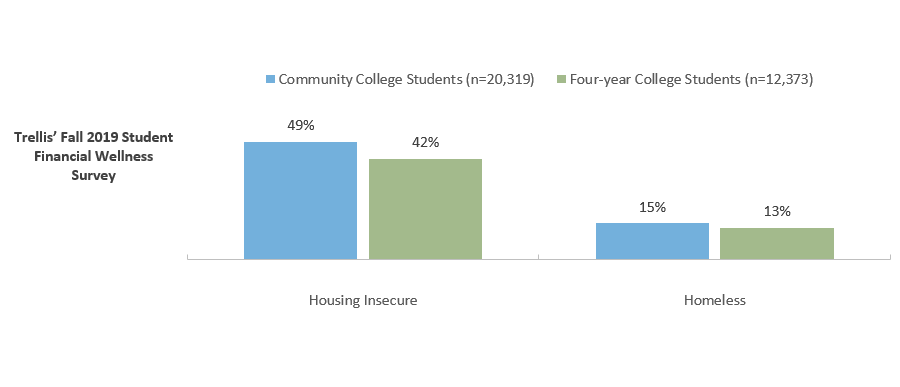

Almost Half of Community College Students are Housing Insecure

Housing Security and/or Homelessness within Prior Twelve Months at Community and Four-year Colleges

Sources: Klepfer, K. Cornett, A. Fletcher, C. & Webster, J. Student Financial Wellness Survey: Fall 2019 ((https://www.trelliscompany.org/student-finance-survey/); U.S. News and World Report (February 27, 2018). A New Focus on College Campuses: Ending Housing Insecurity. https://www.usnews.com/news/education-news/articles/2018-02-27/campus-focus-on-solving-housing-insecurity-helping-homeless-students.

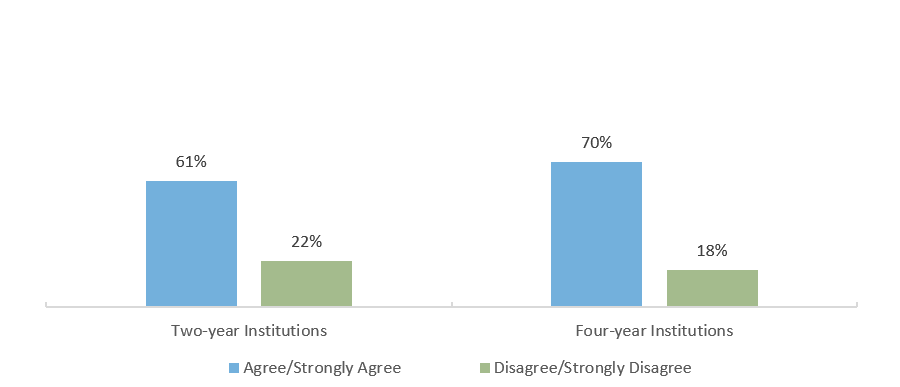

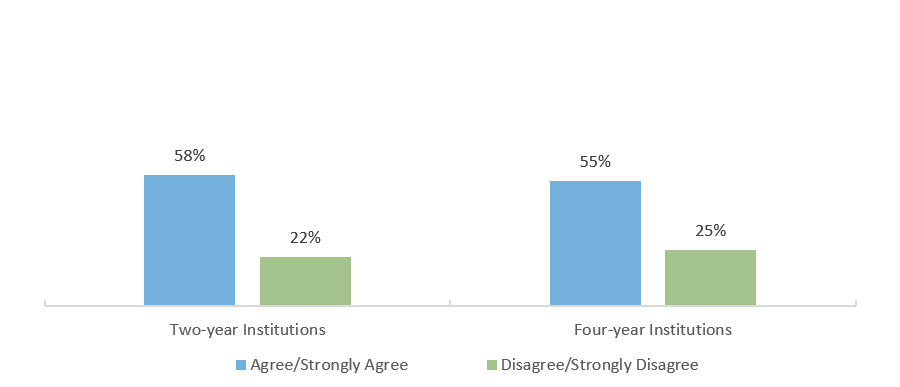

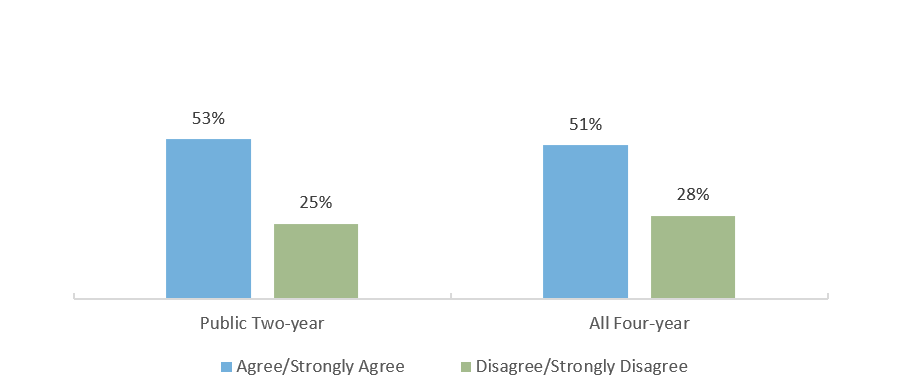

More Than Half of Students Have Concerns About Affording College

Q51: I worry about having enough money to pay for school.*

Q52: I know how I will pay for college next semester.*

Note: Trellis’ Student Financial Wellness Survey is open to any college nationwide that wants to participate. In the fall 2019 implementation, 78 colleges in 20 states participated – 54 community colleges and 24 four-year institutions. There were 23,684 respondents attending public two-year institutions and 14,804 respondents attending four-year institutions. The results are not nationally representative.

*Responses indicating ‘Neutral’ are not shown

Sources: Klepfer, K. Cornett, A. Fletcher, C. & Webster, J. Student Financial Wellness Survey: Fall 2019 ((https://www.trelliscompany.org/student-finance-survey/).

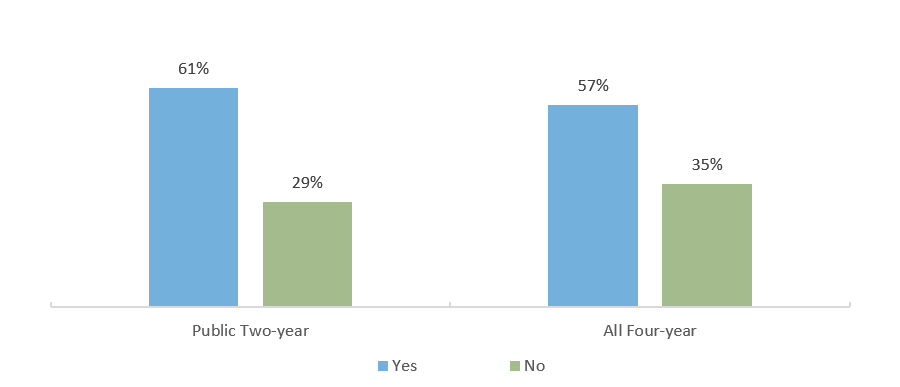

The Majority of College Students Would Have Trouble Getting $500 to Meet an Unexpected Need

Q44: Would you have trouble getting $500 in cash or credit in order to meet an unexpected need within the next month?*

Note: Trellis’ Student Financial Wellness Survey is open to any college nationwide that wants to participate. In the fall 2019 implementation, 78 colleges in 20 states participated – 54 community colleges and 24 four-year institutions. There were 23,684 respondents attending public two-year institutions and 14,804 respondents attending four-year institutions. The results are not nationally representative.

Sources: Klepfer, K. Cornett, A. Fletcher, C. & Webster, J. Student Financial Wellness Survey: Fall 2019 ((https://www.trelliscompany.org/student-finance-survey/); Kruger, K., Parnell, A., & Wesaw, A. 2016. “Landscape analysis of emergency aid programs.” National Association of Student Personnel Administrators (NASPA). https://www.naspa.org/images/uploads/main/Emergency_Aid_Report.pdf.

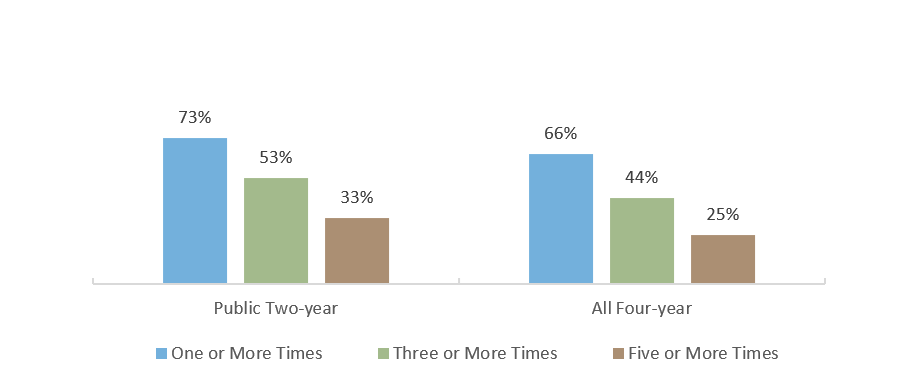

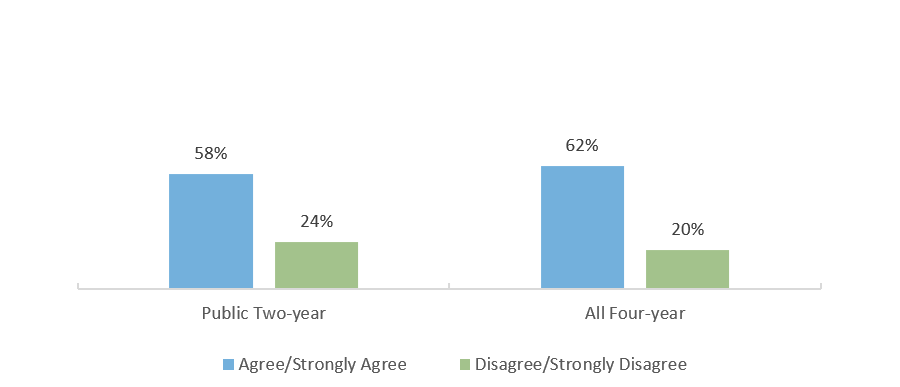

More Than Half of Students Express Concern About Affording Monthly Expenses; Most are Running Out of Money at Least Once Annually

Q50: I worry about being able to pay my current monthly expenses.*

Q45: In the past 12 months, how many times did you run out of money?

Note: Trellis’ Student Financial Wellness Survey is open to any college nationwide that wants to participate. In the fall 2019 implementation, 78 colleges in 20 states participated – 54 community colleges and 24 four-year institutions. There were 23,684 respondents attending public two-year institutions and 14,804 respondents attending four-year institutions. The results are not nationally representative.

*Responses indicating ‘Neutral’ are not shown

Sources: Klepfer, K. Cornett, A. Fletcher, C. & Webster, J. Student Financial Wellness Survey: Fall 2019 ((https://www.trelliscompany.org/student-finance-survey/).

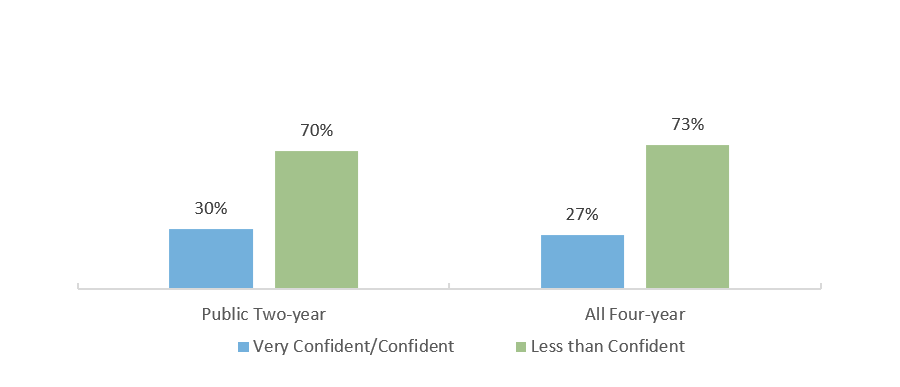

More Than Two-Thirds of Students Are Less Than Confident They Can Pay Off the Debt Acquired

Q69: I have more student loan debt than I expected to have at this point. (of those who indicated having a student loan they took out for themselves)

Q70: How confident are you that you will be able to pay off the debt acquired while you were a student? (of those who indicated having a student loan they took out for themselves)*

Note: Trellis’ Student Financial Wellness Survey is open to any college nationwide that wants to participate. In the fall 2019 implementation, 78 colleges in 20 states participated – 54 community colleges and 24 four-year institutions. There were 23,684 respondents attending public two-year institutions and 14,804 respondents attending four-year institutions. The results are not nationally representative.

*Responses indicating ‘Neutral’ are not shown

Sources: Klepfer, K. Cornett, A. Fletcher, C. & Webster, J. Student Financial Wellness Survey: Fall 2019 ((https://www.trelliscompany.org/student-finance-survey/); Gladieux, L., & Perna, L. (2005). “Borrowers Who Drop Out: A Neglected Aspect of the College Student Loan Trend.” The National Center for Public Policy and Higher Education.

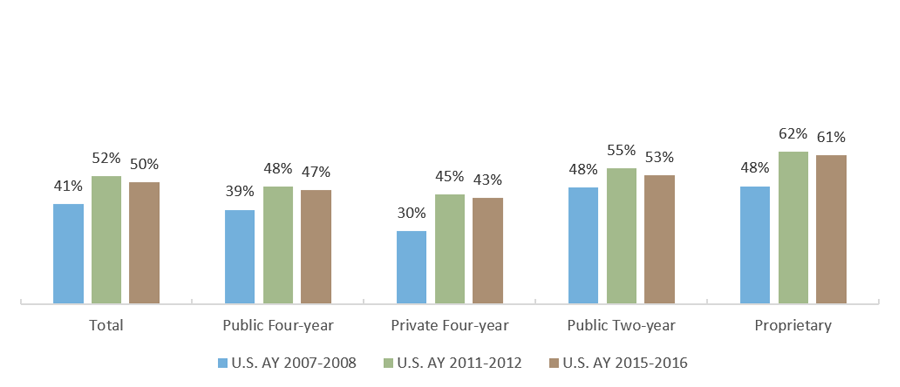

Students at Proprietary Institutions Most Likely to Carry Outstanding Credit Card Balance

Percentage of Undergraduates Nationally Who Carry a Credit Card Balance by Institution Sector (AY 2007-2008, AY 2011-2012, AY 2015-2016)